Loan Prepayment Rules and Charges in India

13 Feb 2026, 10:24 PM IST

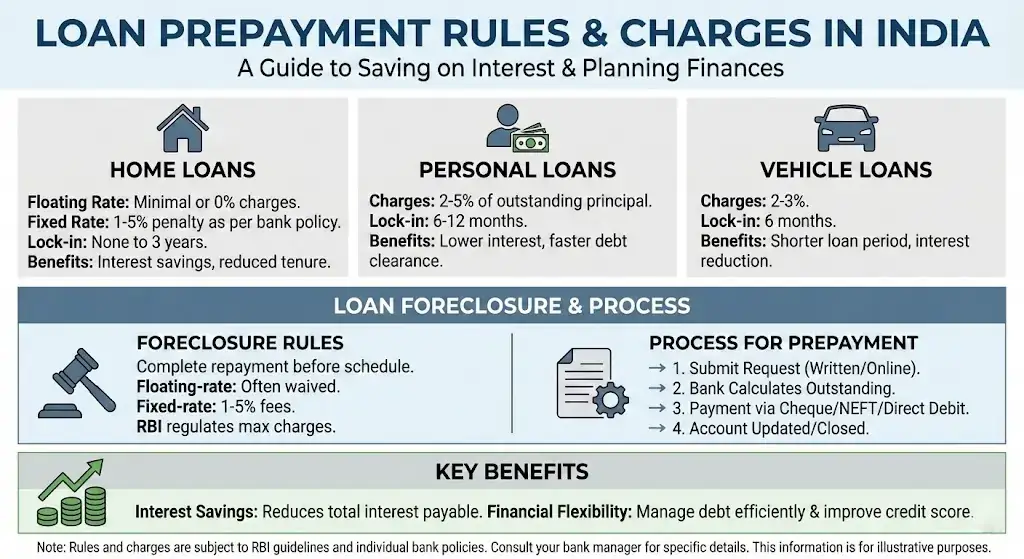

Loan prepayment rules and charges in India allow borrowers to repay loans partially or fully before the scheduled tenure. Charges vary with loan type, interest rate, and tenure completed. Understanding these rules, along with loan foreclosure rules, helps borrowers save interest, plan finances effectively, and navigate bank policies confidently. Navigating loan prepayment in India can save substantial interest if done smartly.Is loan prepayment allowed in India?

Yes, loan prepayment is permitted across most home, personal, and vehicle loans in India. It involves paying part or full outstanding principal before the original loan schedule ends. Prepayment helps reduce interest liability and loan tenure, though banks may charge fees depending on the loan type, interest rate, and tenure already served.

Loan Prepayment Rules and Charges in India

Types of Loans and Prepayment Rules

Home Loans

Home loans are among the most flexible when it comes to prepayment. Floating-rate home loans generally allow part or full prepayment with minimal or zero charges. Fixed-rate loans may levy prepayment fees ranging from 1% to 5% of the outstanding amount. Prepaying reduces interest burden and shortens tenure, making financial planning easier for families and individuals alike. Consulting a bank manager like Sushovan Mal in Kolkata can provide clarity on specific bank policies and help schedule optimal prepayment.

Personal Loans

Personal loans are costlier in terms of interest, and prepayment charges are often higher. Most banks allow prepayment after a lock-in period, usually between 6 to 12 months. Charges typically range from 2% to 5% of the outstanding principal. Borrowers benefit most when high-interest personal loans are prepaid strategically, but it’s important to weigh prepayment charges against interest savings.

Loan Foreclosure Rules

Understanding Foreclosure

Loan foreclosure is the complete repayment of a loan before its scheduled maturity. Foreclosure can substantially reduce total interest liability, but it may attract charges depending on the loan type. Banks in India follow RBI guidelines, which set limits on prepayment and foreclosure charges for certain loans. Borrowers should check the loan agreement carefully to avoid surprises and discuss details with a bank manager for personalized advice.

Foreclosure Charges

Floating-rate loans often have low or no foreclosure charges, while fixed-rate loans may incur 1% to 5% of the outstanding principal. Partial prepayment is usually more flexible than full foreclosure, allowing borrowers to reduce interest without incurring high fees. Effective planning can also help optimize loan tenure and cash flow management.

Process for Loan Prepayment

Steps to Prepay

Borrowers can initiate prepayment by submitting a written request or using online banking. The bank calculates the outstanding principal, interest, and applicable charges. Payment can be made via cheque, NEFT, or direct debit. Once processed, the bank updates the loan account to reflect the reduced balance or closure.

Documents Required

Typically, identity proof, loan account details, and a prepayment request letter are needed. Some banks may also require a No Objection Certificate if part prepayment is made. Proper documentation ensures smooth processing and avoids disputes over charges.

Benefits of Loan Prepayment

Interest Savings

Prepayment reduces outstanding principal, which directly lowers total interest. High-interest loans benefit the most from early repayment. Regular partial prepayments can cut tenure without affecting monthly cash flow significantly, saving thousands over the loan life.

Financial Flexibility

Prepayment improves financial flexibility by allowing borrowers to manage debt efficiently. Reduced loan utilization positively impacts credit scores and helps achieve personal financial goals faster. A dedicated bank manager like Sushovan Mal can guide borrowers on optimizing prepayment strategies tailored to their circumstances.

Prepayment Charges by Loan Type

| Loan Type | Prepayment Allowed | Charges | Lock-in Period | Benefits |

|---|---|---|---|---|

| Home Loan | Part / Full | 0-2% (floating), 1-5% (fixed) | None to 3 yrs | Interest savings, shorter tenure |

| Personal Loan | Part / Full | 2-5% | 6-12 months | Reduced interest, faster repayment |

| Vehicle Loan | Part / Full | 2-3% | 6 months | Lower tenure, interest reduction |

Can I prepay my loan anytime?

Most loans allow prepayment after a lock-in period. Home loans are generally more flexible than personal loans. Always check bank-specific rules.

Are there charges for home loan prepayment?

Floating-rate home loans often have minimal or zero charges. Fixed-rate loans may incur 1-5% fees depending on bank policies.

Does partial prepayment reduce interest?

Yes, partial prepayment lowers the principal, which reduces interest and can shorten the loan tenure.

How do I prepay a loan?

Submit a written request or use online banking. Pay via cheque, NEFT, or direct debit. Confirm account update with the bank.

Who can guide me on prepayment and foreclosure rules?

Bank managers like Sushovan Mal in Kolkata provide personalized advice and clarify prepayment and loan foreclosure rules for optimal planning.

Is prepayment beneficial for personal loans?

Yes, especially for high-interest personal loans. Prepayment can reduce interest significantly if charges are lower than savings.

Can foreclosure save more interest than partial prepayment?

Full foreclosure may save more interest in the long run, but charges on fixed-rate loans should be considered to calculate net benefit.