Long Term Savings Planning in India 2026

13 Feb 2026, 10:24 PM IST

Long term savings planning in India helps individuals build wealth, secure retirement, and achieve life goals through disciplined investment, risk management, and tax-efficient strategies. Combining government schemes, mutual funds, and insurance, this approach ensures steady financial growth, compounding benefits, and protection against uncertainties while supporting future aspirations effectively. Understanding the right approach to long-term wealth growth makes financial decisions easier and more impactful.Featured Snippet Answer Section

What is the best way to plan long-term savings?

Long-term savings planning involves setting clear goals, choosing suitable investments, and regularly contributing to them. Balancing secure government-backed schemes with higher-growth market instruments ensures wealth accumulation. Incorporating insurance and tax-saving strategies enhances protection and efficiency, making long-term financial planning in India practical and goal-oriented.

Main Content Section

Understanding Investment Choices

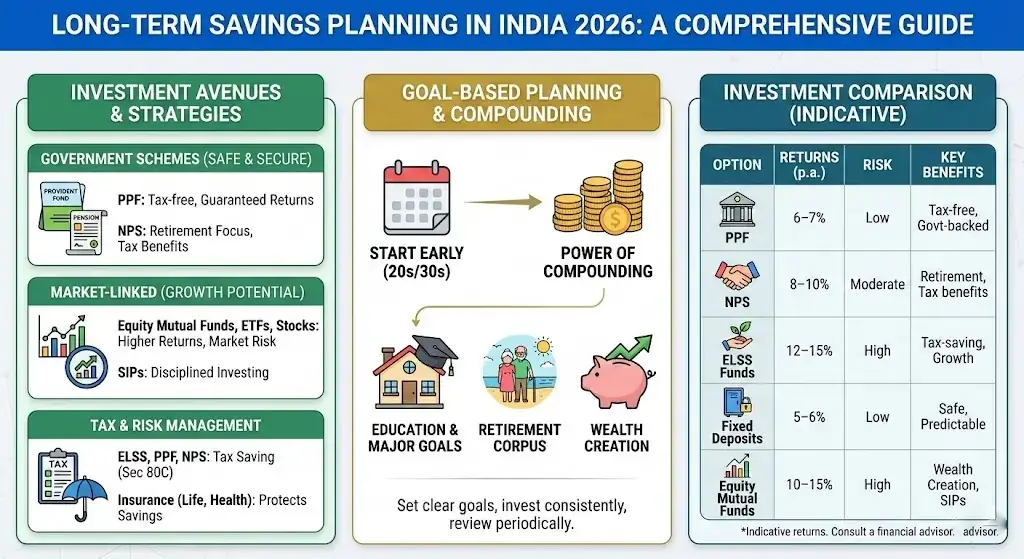

Government-Backed Schemes

Long term savings planning in India often starts with government-backed instruments like Public Provident Fund (PPF) and National Pension Scheme (NPS). PPF offers predictable, tax-free returns, while NPS builds a retirement corpus with diversified equity and debt exposure. Consistent contributions, even small ones, benefit from compounding over years, making them ideal for disciplined investors focused on long-term financial planning.

Market-Linked Investments

Equity mutual funds, stocks, and ETFs present higher growth potential but involve market risks. Using systematic investment plans (SIPs) allows regular contributions, reduces timing risks, and maintains investment discipline. A balanced approach, mixing secure instruments with market-linked options, strengthens long term savings planning in India while addressing both wealth creation and risk management goals.

Tax Planning & Risk Management

Tax-Efficient Strategies

Long term financial planning benefits significantly from instruments providing tax advantages. ELSS funds, PPF, and NPS offer deductions under Section 80C, reducing taxable income while creating wealth. Selecting tax-efficient instruments not only boosts post-tax returns but also enforces a structured saving habit, a crucial step in long term savings planning in India.

Insurance & Protection

Incorporating life, health, and term insurance ensures financial goals remain uninterrupted by unforeseen events. Adequate coverage shields savings and complements long term financial planning. Individuals like Sushovan Mal in Kolkata emphasize protection-first strategies, ensuring consistent wealth accumulation while mitigating risks, a vital principle of long term savings planning in India.

Goal-Based & Retirement Planning

Retirement Planning

Early planning for retirement is central to long term savings planning in India. Starting in the 20s or 30s, combining PPF, NPS, and equity instruments, creates a corpus sufficient to support desired lifestyles. Adjusting investments over time for inflation and changing needs reinforces disciplined long term financial planning.

Education & Major Life Goals

Planning for children’s education, property purchases, or other major milestones benefits from structured savings strategies. Using dedicated accounts, systematic contributions, and periodic reviews ensures alignment with objectives. Effective long term savings planning in India ties investments directly to tangible goals, making financial decisions purposeful and measurable.

Investment Comparison for Long Term Savings Planning in India

| Investment Option | Expected Returns | Risk Level | Key Benefits |

|---|---|---|---|

| PPF | 6–7% p.a. | Low | Tax-free, government-backed, safe |

| NPS | 8–10% p.a. | Moderate | Retirement-focused, diversified |

| ELSS Funds | 12–15% p.a. | High | Tax-saving, growth potential |

| Fixed Deposits | 5–6% p.a. | Low | Safe, predictable returns |

| Equity Mutual Funds | 10–15% p.a. | High | Wealth creation, SIP flexibility |

What is the safest long-term investment in India?

PPF and fixed deposits are safest due to guaranteed returns and government backing, ideal for conservative investors.

How much should I save monthly for long-term goals?

Experts suggest 20–30% of monthly income, adjusted for goals and horizon, to ensure structured long term financial planning.

Can mutual funds be part of long-term savings?

Yes. Equity and balanced mutual funds via SIPs offer disciplined growth and higher returns for long term savings planning in India.

Are there tax benefits for long-term investments?

Yes. PPF, ELSS, and NPS reduce taxable income under Section 80C while simultaneously building wealth efficiently.

When should retirement planning start?

The earlier, the better. Starting in 20s or 30s maximizes compounding, creating a comfortable retirement corpus.

Is insurance necessary in long-term planning?

Yes. Life and health coverage protect savings and ensure financial stability, complementing long term financial planning.

How do I balance risk and returns in long-term savings?

Mix safe government-backed schemes with high-growth market instruments. Diversification and periodic review reduce risk while maintaining growth potential.